Crossing the Chasm: Rising Use of EHRs in Life Insurance Underwriting

Highlights

- Our parent company, Munich Re Life US, recently published results from its third biennial accelerated underwriting (AUW) survey to identify emerging trends in the U.S. individual life insurance market.1

- The survey included responses from 31 life insurance companies with an AUW program in production as of June 2022.

- Mirroring the technology adoption lifecycle, the survey found increasing deployment of AUW programs, as well as a strong uptick in the adoption of electronic health records (EHRs).

- We’re sharing these insights to help EHR developers, health information exchanges (HIEs), and other healthcare organizations understand this new use case and why they should join our EHR+ network.

Key Findings

Growth in EHR Adoption

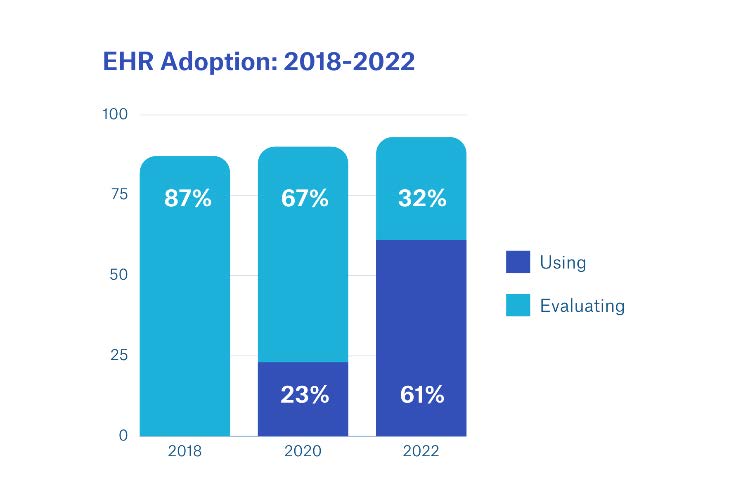

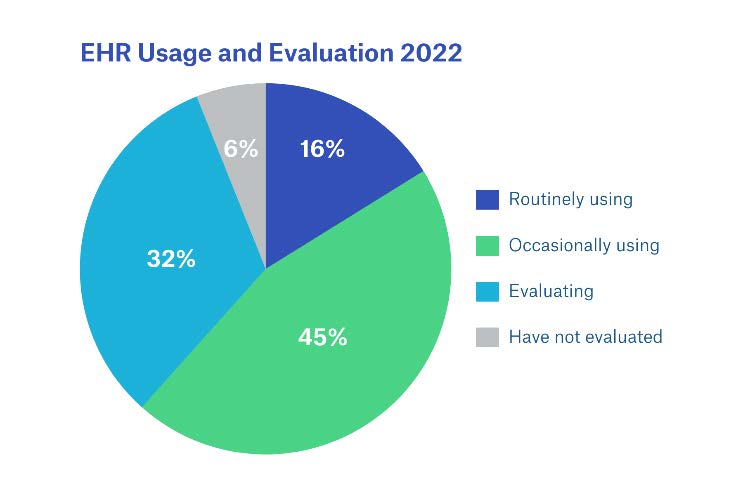

Since 2018, EHRs have been a strategic priority for a large and growing percentage of life insurance companies, a majority of which have transitioned from evaluation to some level of production use over the past few years. Currently, 93% of life insurance companies surveyed are using (61%) or evaluating (32%) EHRs in their AUW programs.

In addition, EHRs enjoyed the largest increase in usage rates since 2020 (+38%) among all digital health data (DHD) sources, exceeding prescription drug data, medical claims, and aggregated laboratory results.

Expansion of EHR Use Cases

Today, EHRs are being used in AUW programs to support specific use cases, including triage, kickouts to traditional underwriting (i.e., referrals for additional underwriting for not meeting other AUW requirements), post-issue audits, and to a limited extent, in AUW rules engines with underwriter review. Going forward, most life insurance companies are planning to integrate EHRs with their AUW rules engines for decisioning without underwriter involvement.

As these use cases mature, life insurance companies that are occasionally using (early majority) or evaluating (late majority) EHRs will have a clear roadmap – combined with all the necessary tools – to make the leap to routinely using EHRs in their AUW programs, catching up with today’s innovators and early adopters.

Proliferation of AUW Programs

Since Munich Re’s first AUW survey in 2018, AUW usage has consistently expanded across products (term, universal, and whole life), face amounts (now approaching $2M of coverage), and risk classes. Key performance indicators including eligibility, acceleration, and offer rates are also improving as life insurance companies seek to optimize straight-through processing (STP) in their AUW programs.2

COVID Impact

The COVID-19 pandemic served as an accelerator for AUW programs. In 2020, many life insurance companies loosened AUW eligibility requirements to make socially-distant, non-invasive underwriting available to a broader pool of applicants. Initially considered temporary, these expansions have not only demonstrated staying power, but also stimulated adoption among life insurance companies eager to keep up with consumer demand for a streamlined purchase experience.

Conclusion

The survey results provide a clear rationale for Munich Re’s strategic acquisition of Clareto last year, with Munich Re concluding:

“Given the importance of reliable medical data in the absence of traditional insurance labs and exams, we think it will only be a matter of time before these emerging DHD sources [including EHRs] saturate the market… In the future, we expect to see human intervention decline and [DHD] sources continue to gain traction as life insurance carriers work towards optimizing their [AUW] programs to issue more policies with faster turnaround times, all while remaining confident in their risk-decisioning process.”

What’s Next

To continue advancing along the technology adoption curve, life insurance companies identified several areas of improvement for EHRs. By joining our EHR+ network – purpose-built for risk assessment via authorization-based disclosures – our health data partners can trust that we’re addressing these needs via the following initiatives:

- Higher hit rates: The EHR+ network achieves an industry-leading patient match rate of >70% nationwide, representing >230M covered lives, while continuous monitoring and optimization of each connection ensures the highest possible performance.

- More complete data: The EHR+ network includes leading EHR developers, HIEs, and other DHD sources, creating important overlaps, offering unmatched breadth and depth, and ensuring that our partners’ data never stands alone.

- Enhanced usability: The EHR+ open partner ecosystem includes integrations with Munich Re’s digital solutions, as well as data normalization, provider directory, and other complementary services, giving life insurance companies the tools they need to get the most out of EHRs.

Please contact us if you’d like to learn more about Clareto and opportunities to join the EHR+ network.

- For this survey, AUW is defined as “the waiving of traditional underwriting requirements (e.g., fluids, medical exams) for a subset of applicants that meet favorable risk requirements in an otherwise fully-underwritten life insurance process.” ↩︎

- The definition of STP may vary from one life insurance company to another, ranging from “AUW decisioning without human underwriter involvement” to “offer[ing] multiple acceleration paths with varying degrees of human touch.” ↩︎