Cost-Benefit Analysis: Quantifying the Value of EHRs

Munich Re Life US assessed the potential value of Electronic Health Records (EHRs) under various assumptions by performing a cost-benefit analysis on a sample of two hundred life insurance applications for which EHRs were ordered post-issue. The mortality savings from using EHR data, had it been used in the risk selection, was compared to the procurement cost of EHRs.

Executive summary

Munich Re’s surveys on accelerated underwriting (AUW) trends among U.S. individual life insurance carriers point to a steep adoption of EHRs: from 0% in 2018, 23% in 2020, to 61% in 2022. Carriers are using EHRs in their AUW programs as a triage tool to refer to traditional underwriting, in post-issue audits, and in AUW light touch, where fast but valuable data can be assessed for risks that kick out due to one of the instant-decision tools. These emerging trends point to the rapid changes happening in the industry and demonstrate how EHRs are well-positioned to revolutionize life insurance underwriting.

This study aims to answer the question: Do EHRs provide value for the money? The paper summarizes a cost-benefit analysis conducted by Munich Re that compared the mortality savings from using EHRs to accurately assess risk versus the cost of procuring the EHRs.

Munich Re analyzed 200 recently underwritten AUW life insurance applications on which EHRs were obtained post-policy issue. Two separate risk class assignments, pre- and post-EHR, were made for each application. Results showed that mortality savings from using EHRs more than covered the EHR cost. A separate analysis of a smaller sample from a different target population also confirmed these results.

Methodology

- Munich Re conducted post-issue reviews on 200 recently issued AUW policies using EHRs obtained from Clareto, a Munich Re company and leading provider of digital health data. The EHRs contained rich, underwriting-relevant longitudinal medical histories such as vitals, smoking history, diagnoses, procedures, lab results, medications, and clinical notes.

- For this analysis, we extracted a subset of readily available digital data from each EHR: height, weight, BMI, blood pressure, smoking history, diagnoses, and select lab results aligned with insurance blood and urine tests and their associated service dates.

- Munich Re underwriters identified cases where the digital data indicated possible applicant misrepresentation and flagged impairments and values of concern. Underwriters reviewed the EHRs for these cases and determined a post-EHR risk class, taking into account the new information from the EHRs.

- The net benefit calculation was as follows: Net benefit = present value of the premium difference between post-EHR and pre-EHR risk class (A) minus EHR procurement cost (B) minus the cost of EHR review by an underwriter (C). This analysis used mortality savings from comparing the post-EHR and pre-EHR risk classes as a surrogate for the present value of the premium differential (A). The cost of EHR review by an underwriter (C) was not part of the analysis.

- Mortality savings were calculated as the present value of future death benefits (PVDB) over a 10-year time horizon based on the post-EHR review risk class minus the PVDB based on the pre-EHR issued risk class. This represented the dollar savings on a present value basis had the EHR been used to assess the risk at the time of underwriting.

- The 2015 Society of Actuaries (SOA) Valuation Basic Table (VBT) without mortality improvement was used as the underlying mortality basis. Lapse and interest rates were set to best estimate assumptions.

- Preferred risk class factors for the four non-tobacco (NT) and two tobacco (TB) classes were set to typical industry factors. Declines were set to 500% of standard mortality.

- The total EHR procurement cost was $11,000, which equated to $55 per applicant.

Study population and results

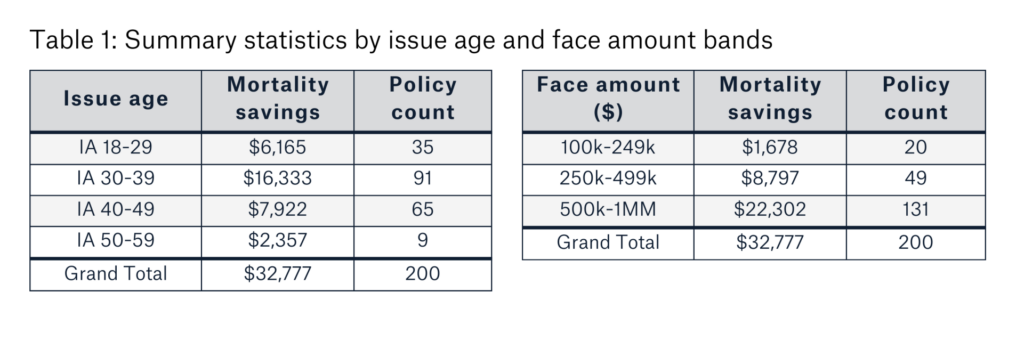

Table 1 summarizes the mortality savings and distribution results by issue age and face amount.

Ninety-five percent of the study population was below age 50. Face amounts ranged from $100,000 to one million dollars. Overall mortality savings were $32,777, translating to an 8.2% mortality load, which more than covered the $11,000 EHR cost. This translated to a $109 net benefit (mortality savings minus cost) per case.

In this population, none of the cases reviewed resulted in an underwriting decline decision. Uncovering even a handful of declines could result in a disproportionate increase in mortality savings.

Mortality savings can vary widely

Munich Re also performed a separate cost-benefit analysis on a sample from a very different target AUW population than the one above. This second analysis was based on less than one hundred cases and had double-digit percent declined risks uncovered by EHRs. Given the significant impact of declined risks on mortality results, the net benefit of using EHRs increased to more than $800 per case for this sample.

Scenario testing and results

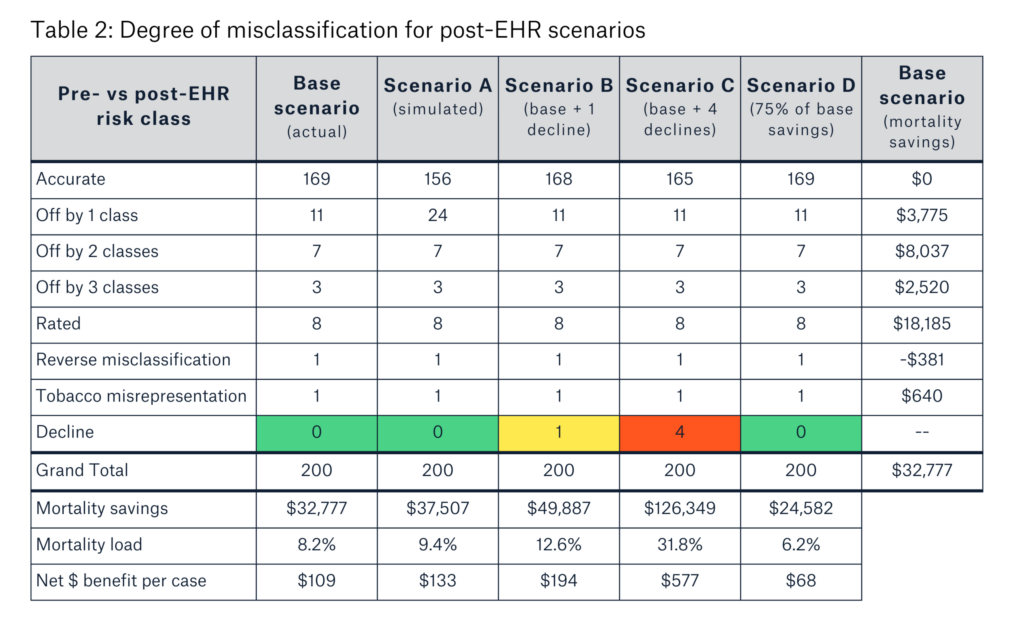

We ran scenario testing on the first sample of 200 cases to simulate the range of outcomes. Table 2 describes how the risk class assignments changed post-EHR for the base and scenarios A to D.

For the base scenario, 55% of the mortality savings accrued from eight cases transitioned from standard or better non-tobacco pre-EHR, to rated non-tobacco post-EHR. Vitals (BMI/build and blood pressure) and undisclosed adverse impairments were the top two drivers of misclassification.

Scenario A had an additional 13 cases transition from a previously accurate assessment to the next-worse post-EHR risk class to simulate more extensive use of EHR data. Scenario B, with one case moving from standard to decline, showed the impact of identifying one decline. Scenario C, set to a typical decline rate of 2% in post-issue audits, had one best-preferred best case, one preferred case, and two standard cases all move to decline.

Scenario D attributed 75% of the base-scenario mortality savings to the EHR. This simulated the scenario where less new evidence was discovered from the EHR. In other words, there was a higher amount of overlap between data in the EHR and other underwriting requirements already used at the time of underwriting.

Considerations

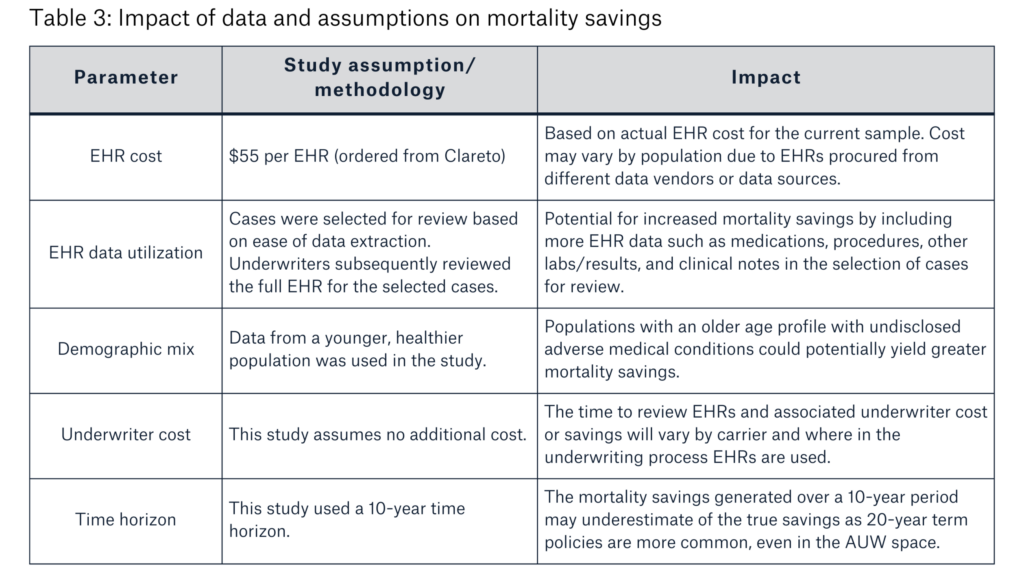

Table 3 outlines the potential impact of the data and assumptions used in this cost-benefit analysis on the results.

AUW programs vary by program parameters, the types of underwriting tools and data sources used, and how those tools are applied. Additional factors impacting the mortality savings results include face amounts, preferred risk class distribution, other underwriting requirements, target market, and treatment of reverse misclassification.

Conclusions

Overall, Munich Re concludes that EHRs provide value for the money.

The cost-benefit analysis in this article provides quantifiable evidence that the additional mortality savings from EHRs, even accounting for other tools in accelerated underwriting programs, is greater than the procurement cost. The results also point to a potentially wide range of mortality savings.

With increasing hit rates, faster procurement times, and more actionable information resulting in faster decisioning, EHRs are well-positioned for widespread adoption in life insurance underwriting. This is particularly prominent in the accelerated underwriting environment where managing misrepresentation risk and mortality slippage is critical for program success. From our review and analysis, we see that EHRs can provide detailed and verifiable medical history to mitigate misclassification risk.

In addition, as the results of this cost-benefit analysis show, with industry AUW trends of increasing face amounts, even uncovering a handful of adverse medical history cases by EHRs is enough to provide bang for the buck.

Carriers should consider comparing the mortality savings from using EHRs against their unique program features and cost structures to assess the value of using EHRs on their block of business. Munich Re Life US and Clareto can work with carriers on ideas for incorporating EHRs in their underwriting process.